Mon, June 02, 2008

Mutual Funds and Fees

How much do you pay each year in mutual fund fees? Investors who ignore this question stand to lose a considerable percentage of their investment returns over the long-term.

It’s not what you make, but what you keep, that matters in any investment. Mutual fund fee structures can be confusing. In principle, a “load” fund can charge a new investor as much as 8.5% . So, for example, if the investor rolls $100,000 from an old 401(k) into an IRA and invests the money in a fund with a 5% front-end load, his investment is instantly worth $95,000. In order to recover the fee, the investment must gain a 5.26% (yes, slightly more than the fee paid!) just to break even.

Recently, a client who made an investment prior to hiring me described how upset he was when he discovered how much he was paying each year in fees for the investment. Irrespective of performance, his investment was being clipped by 2% of its value each year. Somehow he hadn’t been made aware that this investment involved an ongoing fee. I suspect that his situation isn’t unusual.

Many investors have figured out that “no-load” mutual funds are usually preferable to load funds. However, even no-load funds involve annual fees; these may be called 12(b)-1 fees, management fees, or something else. The effect of fees on no-load funds is important, though recognizing their impact can be difficult. Many people don’t intuitively grasp the effect of compound interest on their returns, but this is just the effect that is in play where mutual fund fees are involved.

The impact of these fees is also hard for the average investor to understand because the fees are deducted directly from the fund’s net asset value. You don’t write a check for 12(b)-1 fees, nor does the mutual fund company note a debit in your personal account statement to reflect the cost. Nevertheless, you do pay. Paying the fee this way is less psychologically painful than writing a check, perhaps, but the impact on your net worth is no less real.

In principle, 12(b)-1 fees (named after the SEC rule that authorizes mutual funds to charge them) compensate mutual funds for expenses such as marketing and selling shares, compensating brokers or others who sell the fund shares, and paying for advertising and sales literature. In practice, the fee can be hard to rationalize; for example, funds that are closed to new investors can still charge 12(b)-1 fees, though presumably since the fund is not being marketed to investors, marketing expenses should be negligible.

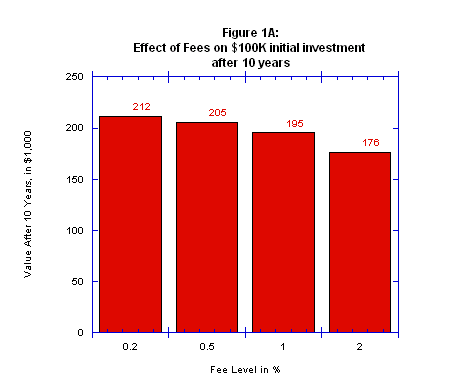

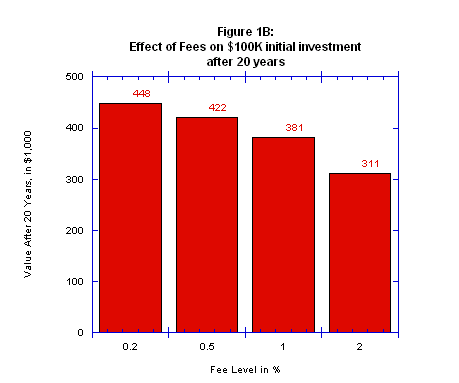

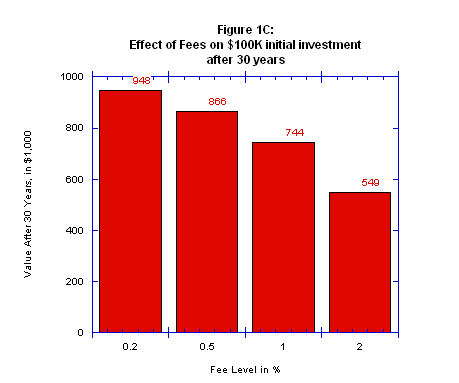

In any case, the effect of these fees is significant over time. Annual fees for “no-load” stock mutual funds typically range from 0.10 % to 2.3%. Figure 1A shows how $100,000 invested in a mutual fund would grow after 10 years of 8% annual returns under various fee structures. The amount an investor has at the end of 10 years is quite sensitive to fees. Figures 1B and 1C illustrate the same effect for investments held for 20 and 30 years, respectively.

Not surprisingly, the longer the investment term, the greater the impact of higher fees.

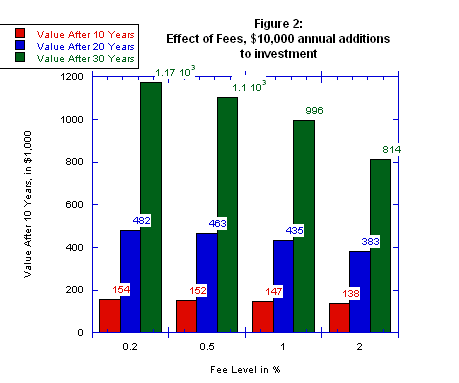

Figure 2 provides similar results for scenarios in which, instead of investing a single lump sum, the investor makes regular annual investment of $10,000 at the beginning of each year (I’ve plotted the 10, 20, and 30 year results in a single figure this time) with 8% annual returns. Again, the “fee drag” on ultimate investment returns is evident.

Investment managers who charge relatively high fees will usually argue that this sort of analysis is flawed in its assumption that the investment returns are the same at all fee levels. It’s claimed that the higher fees are merely fair compensation for higher returns. However, studies have shown that over the long run, higher mutual fund fees rarely track with higher returns for the investors.

Despite this fact, many investors really want to believe that higher fees will result in higher returns, even when they have access to data that indicates otherwise. Three researchers at the Wharton School of Business, Harvard, and Yale did a study of students at Wharton and Harvard and found that when given a range of fund options, they did not necessarily choose to invest in the funds with the lowest expense ratios, despite the fact that the funds were otherwise identical.

The question of “active” versus “passive” mutual fund management is related to this cost issue, as actively managed mutual funds tend to charge higher fees. I hope to address this in more detail, but it will have to wait for a future post.

It should be clear, though, that the annual fees paid for a mutual fund (or exchange traded fund, variable annuity contract, or other investment product) have an enormous impact on an investor’s return. This is a truth that marketers of the more expensive investment products don’t like to discuss, but prudent investors need to keep it in mind. What you care about, after all, is how much you have after expenses, including taxes (tax effects, alas, will also have to be addressed in future posts!).