Tue, May 27, 2008

The Housing Market is Up! No, It’s Down!

Mark Twain is credited with saying a great many things that he may or may not have actually said. Among these is the observation that "People commonly use statistics like a drunk uses a lamp post: for support rather than illumination." If Twain did say it, he might have had housing statistics in mind. If you pay attention to news reports, you're likely to hear widely-varying assessments of the state of the housing market. Who's right?

One of the challenges in interpreting housing market statistics is that some of the key sources of housing information have a vested interest in putting a positive spin on the data. For example, you can generally count on the National Association of Realtors (NAR) to find an interpretation leading to the conclusion that housing markets are "looking up."

Of course, this is done partly because housing markets are sensitive to the public mood. No authoritative source wants to announce that housing is tanking for fear that the news media will repeat it endlessly until it becomes a self-fulfilling prophecy. I recently attended a talk given by Robert Shiller of Yale (and MacroMarkets LLC) on speculative excesses and the subprime crisis. He began his talk with a slide bearing a lengthy legal disclaimer in bold print, then apologized for it. It seems that in a presentation to a New Haven social club in April, Shiller had incautiously expressed pessimism about the housing market and his remarks were picked up by the press and greatly amplified. His business partners consequently made him vow not to make any public comments about the direction of the housing markets (especially since his firm is in the middle of trying to register a new financial derivative product related to housing prices, and the SEC can be touchy about such statements).

Another difficulty relates to the old saw about the three most important factors determining the value of a house ("location, location, and location"). The price of a house is strongly influenced by the municipality or even the neighborhood in which it exists. It's hard to say that "the market" has recovered when there isn't really one market; there is great diversity among housing markets in different places.

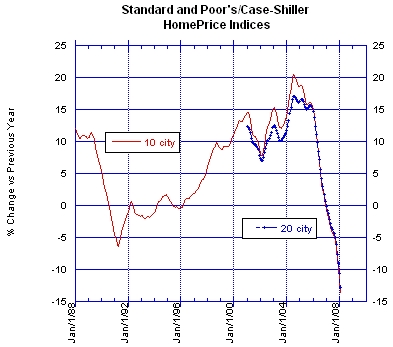

One measure of housing markets behavior is the Standard and Poor's/Case-Shiller home price index, which looks at the prices of single-family houses that have sold at least twice, thus allowing an analysis of how individual home values have changed. Like the many indices that exist for financial markets, the S&P/Case-Shiller Index gives a big-picture indication of how US housing markets are doing. There are actually two versions of the index; one is based on housing sales prices in ten cities, the other uses data from 20 cities. The most recent data indicate that housing in many major cities is, er, tanking.

As shown in Table 1, half of the cities in the 20-city composite index have experienced double-digit price declines vs. a year ago (data through Feb. 2008).

Table 1: Major Downers

| Detroit | - 16.5 % |

| Las Vegas | - 22.8 % |

| Los Angeles | - 19.4 % |

| Miami | - 21.7 % |

| Minneapolis | - 12.5 % |

| Phoenix | - 20.8 % |

| San Diego | - 19.2 % |

| San Francisco | - 17.2 % |

| Tampa | - 17.5 % |

| Washington, DC | - 13.0 % |

| Source: Standard and Poor's data online | |

Among the other cities in the 20-city composite (Atlanta, Boston, Charlotte, Chicago, Cleveland, Dallas, Denver, New York, Portland, and Seattle), only Charlotte, NC showed a one-year increase. Using Standard and Poor's numbers, Boston-area single-family prices are down a mere 4.6% from last year. But the big picture is that many housing markets are swooning, and it's not obvious that things have bottomed out yet.

Ever-optimistic, the number-crunchers over at the National Association of Realtors have been eager to point out in their press releases that median home prices are actually up in about a third of the cities in their survey, suggesting (to them, anyway) that prosperity is just around the corner. A close look at the NAR data reveals that the cities with rising home prices tend to be much smaller than the metropolitan areas in the Case-Shiller index. Prices are rising in towns like Buffalo, El Paso, Binghamton, NY, Peoria, and Greenville, SC. These are places that aren't economically unimportant, to be sure, but they represent a much smaller segment of the population than the cities in the S&P/Case-Shiller index.

So not all housing markets are down, but the major trend is negative. Cities with rising prices appear to me to be places whose housing markets were undervalued relative to the rest of the country for a long time, and now they're catching up. The NAR also reports that the median US single-family home sale price has declined to $196,300 in the first quarter of 2008.

Closer to home (for me), there are indications of a continued slowdown. The number of single-family home sales in MA was down almost 23% in February, and the Boston Business Journal reported recently that this will be the slowest year for new residential construction in Massachusetts since 1982. In February, home-building permits were down 50% vs. last year.

Yet even with a statewide downturn, there are localized exceptions. Home sales were either flat or up in 34 Massachusetts towns in the first quarter of 2008, though evidence of firming prices is hard to find. With lots of relatively small towns and cities in the state, the picture is further clouded by the fact that real estate numbers can be skewed by the relatively small amount of data.

What does all this mean? I think it means we can expect a continuation of weak housing markets nationwide, with bright spots here and there (even in over-priced states like Massachusetts). In areas where housing prices didn't rise as rapidly as the national average over the last decade, housing prices may strengthen, especially if the local economies are strong. Yet even these markets must fight an uphill battle as banks impose tighter lending standards on all kinds of debt, including not only real estate loans, but also student loans and credit cards. Markets with higher-priced housing are selling more slowly than other parts of the country, and areas with above-average foreclosure levels are likely to have depressed housing prices for a while to come. Realtytrac.com has a nice map showing foreclosures nationwide; the red areas have the highest levels of foreclosure.

The likely direction of real estate will have to be discerned locally. So, for example, when you see that Boston area banks report a surge in loans gone bad , business bankruptcies have shot up, and Massachusetts' state treasurer gave a rather cautious assessment of state finances to the local Chamber of Commerce last week, none of this points to an imminent recovery in housing. Housing in Massachusetts should eventually recover if job growth continues, but all indications are that a significant upturn in prices is unlikely in the next couple of years. The last downturn in MA real estate took almost a decade to unwind fully.